Ethena Monthly Reserve Fund Recommendations: September

Summary

This analysis is presented by LlamaRisk and Blockworks Advisory, members of the Risk Committee leading risk recommendations on the Reserve Fund. We will periodically re-evaluate the fund’s size based on market conditions, changes in USDe’s backing, and projected capital needs, with the previous monthly update published in August.

The overall situation over the last month was positive, with USDe supply growing to ~$14.3B, primarily fueled by further expansion of Ethena ecosystem and deployment and rather positive market situation. Nonetheless, the funding rate yields and overall market yields, including PT assets, lowered over the past week. All things considered, the direction for the near future remains positive, with more ecosystem expansions expected to attract new USDe supply.

LlamaRisk’s methodology suggests a need for $56.1M on the conservative scenario and $41.1M on the moderate side, while Blockworks Advisory recommends $55.5M. What led the recommended capital not to surpass the current fund size (~$62M) is the fact that Ethena did not allocate incremental backing to perpetual futures positions. Therefore, the current fund size is sufficient to support the current USDe supply. We will conduct more continuous internal reviews to ensure this insurance buffer remains adequate for USDe’s continued stability.

Reserve Fund Composition

The Reserve Fund is currently composed of the following assets, totaling approximately $61.84M:

- $41.8M worth of USDtb

- Curve USDtb–USDC pool position of $19.9M (10M USDC and 9.9M USDtb)

The composition has changed due to the accepted proposal to consolidate all Reserve Fund assets into USDtb related assets. This was approved as of last month and mentioned in the previous monthly update.

LlamaRisk Methodology & Estimations

Utilizing the Reserve Fund drawdown methodology developed by LlamaRisk, which considers current and historical market conditions, USDe collateral distribution, stablecoin buffer, and sUSDe supply, we present up-to-date drawdown simulations to estimate current Reserve Fund capitalization needs.

Conservative Scenario

In this scenario, according to the methodology, we assume all perpetual positions would need to be closed within a 24-hour time span, incurring 50 bps in negative funding rate losses and 50 bps in slippage losses. From this, we derive the following estimate for the required Reserve Fund size:

Source: Reserve Fund Drawdown Methodology V2, September 24, 2025

Simulating this short-term risk scenario results in a currently recommended Reserve Fund size estimation of $56.1 million. With this Reserve Fund size, Ethena would remain solvent and be able to serve all USDe redemptions, even under the worst tail-risk scenario that would require closing all perpetual positions in a short time frame.

Moderate Scenario

The moderate scenario assumes that a decline in funding rates would trigger a significant amount of sUSDe to enter the unstaking queue, leading to a potential wave of USDe redemptions. The maximum amount of USDe is based on the current circulating supply and the assumption that USDe in liquidity pools will not be redeemed. It is also assumed that Ethena will prioritize timely redemptions to prevent the USDe price from de-pegging, using its stablecoin buffer for instant redemptions and closing perpetual positions for the rest. Additionally, the scenario assumes that redemptions requiring the closure of perpetual positions will be managed with slippage capped at 75 basis points and funding rate losses limited to 5 basis points, while any remaining positions could face up to 50 basis points in funding losses before being gradually wound down with lower slippage.

Source: Reserve Fund Drawdown Methodology V2, September 24, 2025

This scenario results in a currently recommended Reserve Fund size of $41.1 million. With this Reserve Fund size, Ethena could successfully manage a significant redemption event by utilizing its liquid buffer, tapping into the available money market liquidity and unwinding some perpetual positions without incurring excessive slippage, allowing for a more gradual and orderly unwinding of positions if necessary.

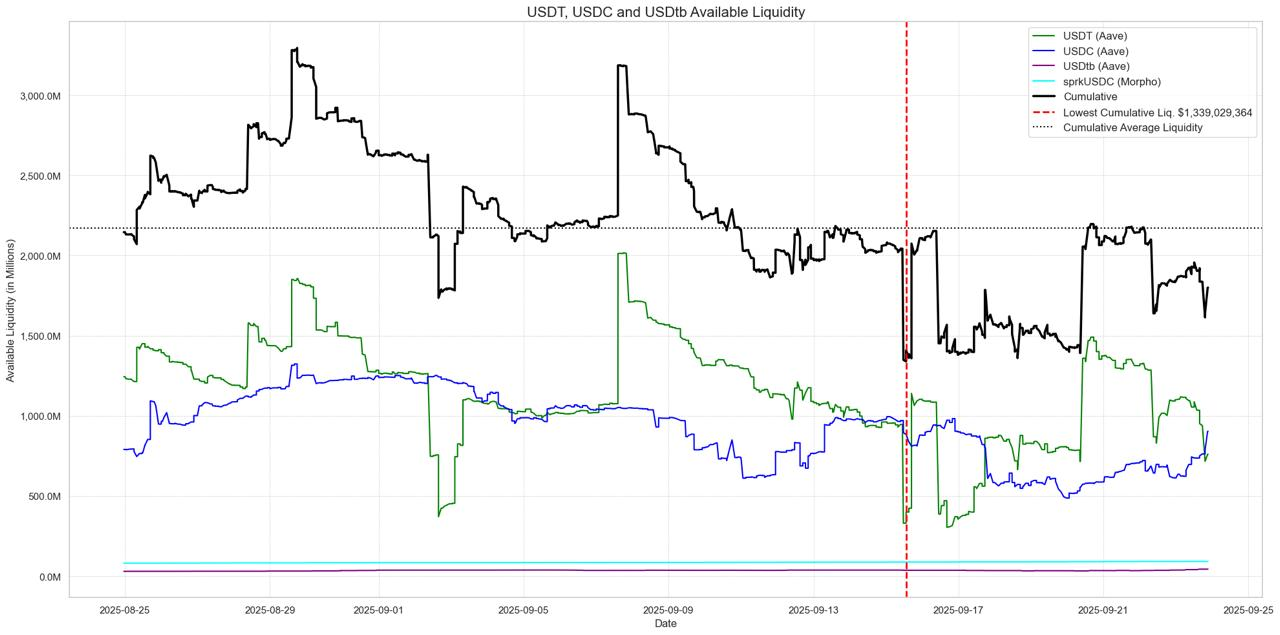

The available free liquidity buffer is also impacted by the availability of liquidity in pools where Ethena has sizeable supply allocations, notably USDC and USDT on Aave. Based on an analysis of on-chain data, the 30-day cumulative average available liquidity for the supplied assets is approximately $2.1B. While the effectively illiquid part can impact the buffer available to service redemptions, we have also found that incremental redemptions would be tied to the loan repayments in the same Aave pools, freeing up liquidity before redemptions are serviced. We will publish in-depth findings of this analysis in a separate post.

Source: LlamaRisk, September 24, 2025

Blockworks Advisory Methodology & Estimations

Assuming a highly conservative scenario where Ethena chooses to unwind all perps positions within 24 hours during a severe market downturn, the Reserve Fund needs to cover two key costs: negative funding rates during that window and slippage from exiting positions. Note that the likelihood of requiring 100% position closure in 24 hours is very low and this scenario addresses a worst-case possibility in terms of funding rates.

To estimate funding costs, we can use a dynamic model that builds on the approach of looking at the share of backing in perpetuals by also factoring in the specific assets and venues involved, allowing for a nuanced assessment. The model considers the most extreme historical funding events, specifically the worst 0.1% of datapoints for each asset and exchange pair, and applies those rates to Ethena’s current allocation to estimate potential funding cost exposure under stress. This becomes especially important as more volatile collateral assets like SOL are added, and as certain venues prove better equipped than others to handle extreme market conditions. The same total allocation can carry very different risk profiles depending on where and how it’s deployed, which in turn affects the size needed for the Reserve Fund.

Slippage is the second major cost, incurred both when closing short positions and selling spot. We estimate this at 50bps in a worst-case scenario, which was the maximum slippage observed by Ethena when trading ETH perpetual futures during the recent Bybit hack.

Current Estimation and Historical Context

Based on this methodology, the Reserve Fund would today need to currently hold approximately $55.5M to be sufficiently capitalized. At this level, Ethena would be able to fully unwind its current positions even under historically extreme negative funding conditions, while maintaining solvency throughout.

To put this into perspective, consider the estimated Reserve Fund requirement as a percentage of total backing. It highlights how the composition of assets can significantly influence the appropriate size of the Reserve Fund, even proportionally to total backing. While current estimates suggest that the Reserve Fund’s needs are below its current capitalization, it’s important to note that Ethena is expected to act swiftly to capture the highest yields available.

Recommendation

According to the consensus of recommendations, the current Reserve Fund size of ~$62M is sufficient to cover potential drawdowns as outlined in our modeled scenarios. This means that no immediate capitalization increases are needed for the Reserve Fund.

While no new allocations are needed at this time, the growing share of USDe backing on Aave and Morpho represents a new dynamic that requires continuous monitoring. The available on-chain liquidity could become a bottleneck during extreme market stress, and this buffer could be exhausted. We will continuously monitor the backing and liquidity dynamics to recommend Reserve Fund increases when needed.